Earnings Trading Platform

An earnings-trading research platform built to answer one question per print: was the edge real?

- Replay

- every print re-runs through the full pipeline

- Walk-fwd

- backtests over the live ticker universe

- A/B

- champion vs challenger engine promotion gates

- Paper-first

- no live capital until the edge is proven

01 / What it is

Trading around company earnings prints, one event at a time.

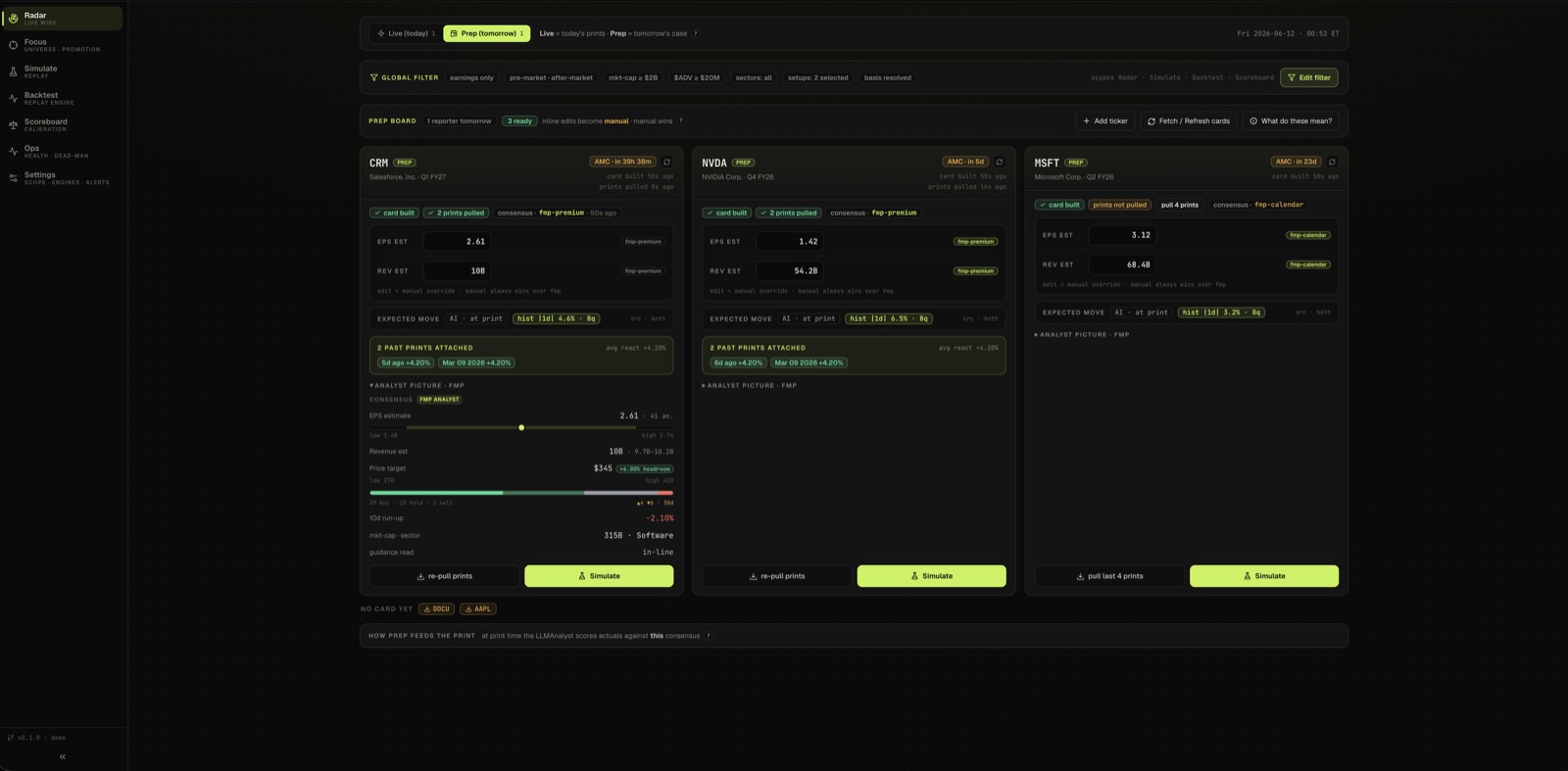

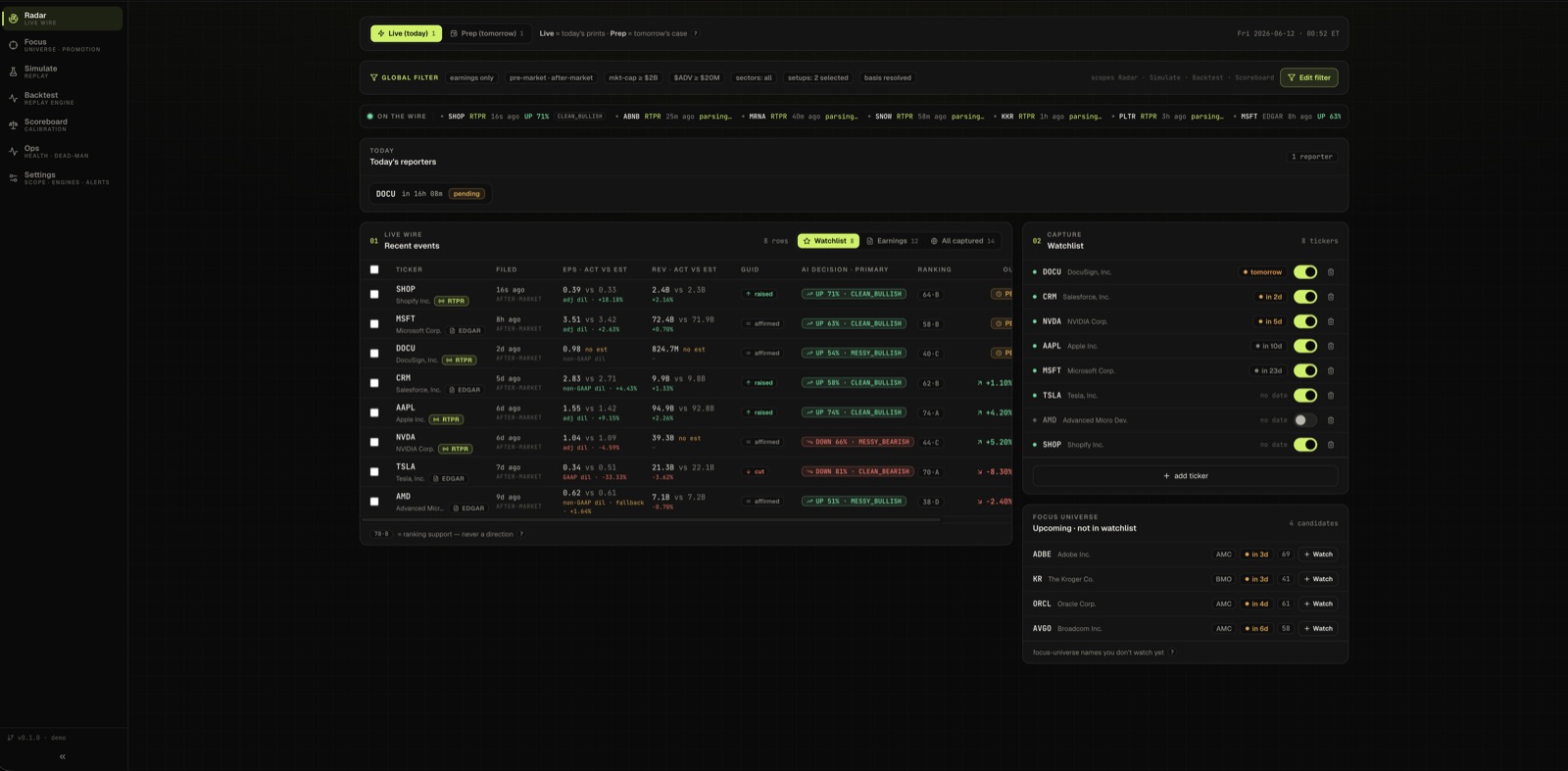

An independent research platform for trading around company earnings prints. A radar tracks upcoming prints across a watchlist; each ticker gets a prep board assembled before the event — consensus EPS and revenue estimates, the options-implied expected move, past print reactions, and an analyst picture — so every decision starts from the same structured context.

02 / Replay, gate, repeat

The simulator re-runs any historical print through the full pipeline.

Every pass runs the full pipeline — filing detected, parsed, features extracted, signals scored, outcome reviewed. Engines compete champion vs challenger: a new configuration (including LLM-driven variants) must beat the incumbent across graded replays before it earns promotion, and calibration gates decide which engines are eligible to act at all. Backtests run walk-forward over the same universe, with per-trade replay results to inspect.

03 / Paper first, by design

The system measures before it trades.

Like its sibling research platform, it runs in shadow and paper modes only, with a reviewable trail for every decision. The research is still in progress — this page is an early preview, and the full case study lands when the methodology closes. Code available on request.

04 / The gate to live capital

This system does not trade real money yet — on purpose.

Before a single live order, the edge has to survive validation end-to-end: replayed prints, walk-forward backtests, and champion/challenger runs that hold up out-of-sample, net of fees, slippage, and the adverse selection that quietly kills paper edges. Until that bar is cleared, everything runs in shadow and paper modes. The project is in active development; if the edge proves real, it goes live small and measured — and if it does not, the postmortem will say so honestly. Either outcome is a result.

05 / The system, end to end

Estimates and filings feed the prep board; engines compete, every print replays, and live capital stays locked behind the gate.

Want the full story once the research closes? Code walkthrough available on request — get in touch.